An article for Alexander Forbes clients appeared in Money Web and the Citizen this week: https://www.moneyweb.co.za/news/markets/all-cycles-turn-eventually/

- COVID-19 is the trigger, not cause, for global recession

- Volatility and risk repricing after years of complacency

- Long-term asset class return expectations improve

- Coast is not clear in short term

- Value in South African real interest rates

- Ripe conditions for active management and hedge funds

We have warned about volatility and low investment returns for a long time. The coronavirus is just the trigger to take the global economy and financial markets into a period of correction, lower returns and heightened volatility. We are never likely to predict the exact cyclical trigger and we did not predict the virus. However, we were aware of the underlying imbalances in financial markets and the global economy pointed towards the need for this correction well before the coronavirus ensued. While painful correction is what we require to generate a better and more sustainable outlook, long-term return expectations are improving, but we are still cautious and expect further challenges over the coming quarters.

We cannot avoid our problems forever

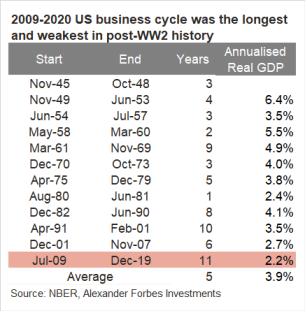

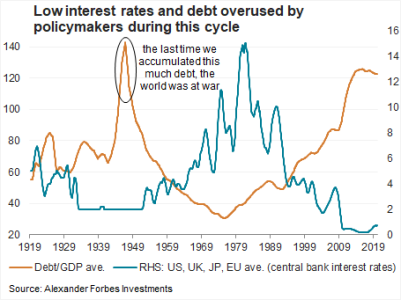

After the longest and weakest economic expansion cycle on record, the United States (US) economy will enter a recession in 2020. The 2009-2020 cycle was 11 years compared with the post-World War II average of five years, and real GDP expanded 2.6% annualised during this cycle compared with the post-war average of 3.9%. It seems contradictory, but one of the reasons for the uncharacteristically weak cycle was deliberate attempts to avoid a recession. Policymakers used low-interest rates and debt to stimulate the economy as much as possible. Developed market interest rates fell to their lowest levels on record during the most recent cycle and debt to GDP levels are at their highest levels since World War II, which highlights the overuse of monetary and fiscal policy. This is not just a US or developed market phenomenon. South African interest rates also fell to their lowest levels on record during this cycle and debt levels to its highest.

Hiding behind debt creates risks and complacency

Debt suggests a preference for consuming today, rather than in the future. This makes today feel better than it should, for example, a weekend shopping binge on credit. Persistent use of debt and interest rates is unsustainable. It is also dangerous because the low cost of debt induces less sensible investment and spending decisions. For example, cheap debt can make a risky business venture seem profitable, an expensive luxury car seem affordable or a leveraged investment into a speculative asset class seem prudent. These errors build up before recessions like deadwood that builds between forest fires. Regular forest fires burn off the deadwood, allowing the ecosystem to rejuvenate quickly and remain healthy. Regular intervention to postpone short-term difficulty leads to a build-up in deadwood and greater pain when it finally ignites. Regular forest fires cause risk to be priced correctly and a healthy dose of scepticism keeps risks in check, whereas the longer the cycle extends, the greater the degree of complacency. The built-in economic errors reduce productivity, which is a major and underappreciated cause of the declining trend in global economic growth.

During the boom times, it is challenging to see the deadwood, but once the correction emerges it is easily visible. Numerous countries and corporates will have their credit risk downgraded during this recession. These downgrades should have taken place many quarters before the recession but low global interest rates and reduced global volatility made the more inflated credit ratings seem palatable. South African and UK government debt downgrades in March 2020 are just two examples of this dynamic.

Cyclical challenges dictated defensive positioning

The late stage in the economic and financial market cycles advocated a defensive position over recent quarters. Nevertheless, absolute return performance for most investors is likely to be poor and tough to digest. Amongst South African asset classes, only nominal bonds and cash beat inflation over the past five years. Globally, returns were still poor but were assisted by 8% annualised US dollar gains against the rand over the past 5 years. Despite the benefit from offshore exposure, the real return experience for South African investors over the past 5 years is comparable with the rare negative returns experienced around 1992 and 2012. This graph shows the performance of a generic regulation 28 South African pension fund portfolio with 45% in SA equity, 25% in SA bonds, 20% in global equity and 10% in global bonds.

Prospects improve as we uncover errors

The long-term return outlook improves as equity market prices correct lower. It is by uncovering our problems and admitting that they exist that we can solve them and invest in a better future. Real return 5-year expectations on global equity recovered to 7% annualised at the end of March 2020, while South African equity expectations recovered to 5%, which is encouraging but not outlandishly cheap. South Africa’s weak economic growth outlook remains a constraint for South African equity. A better long-term return outlook does not eliminate the possibility of further short-term pain.

Ripe conditions for active management and hedge funds

Asset managers that make it through the next few months should outperform their benchmarks over the coming years, seizing on market dislocations. Hedge funds have benefited in these conditions and added value. In contrast to active management, many global exchange traded funds (ETFs) have experienced uncharacteristic illiquidity lately. It is frustrating for investors to experience illiquidity within vehicles that were sold for their liquidity characteristics.

Externalities of falling developed market bond yields

Illiquidity has become a challenge with major US fixed income markets too. We will remain circumspect on the broader market outlook until these US dollar funding challenges alleviate. The weak growth and low interest rate outlook have resulted in a dramatic fall in developed market bond yields. The lower these yields fall, the more pressure on the long-term return outlook from these bonds, which poses a challenge for pensioners and insurers in developed markets. At some point these lower yields will force investors to take allocations elsewhere. Non-growth sensitive store-of-value assets like precious metals are a likely beneficiary.

Extreme real rate differentials in South Africa

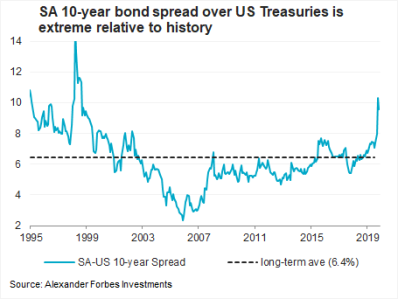

The dramatic weakening in South African government bonds makes the real yields attractive. South African bonds are yielding more than 10% above their US counterparts and could return above 5% real annualised returns over the coming years. The South African rand blew out to R19/$ in early April 2020 – its highest levels on record and two standard deviations away from its purchasing power parity valuation. Challenges within US funding markets imply that the pressure could remain on the rand in the short term, but this type of extreme currency valuation is noticeable and an opportunity for some.

Opportunistic value emerging but caution still advised

Global authorities will try to circumvent the economic and market correction through doubling down on low interest rate policies and expanding government balance sheets. We are aware that these can buoy financial markets over the short term but also cognisant that these policies reduce the long-term growth potential because they intervene with the market-clearing mechanism and reallocation of capital, which is so desperately needed. These policies have already been overused, so the market should be more sceptical when assessing their efficacy. There is a balancing act between long-term opportunities, shorter-term risks, much needed corrections and policymakers who want to avoid adjustment. We continue to balance these factors, through our risk management framework, allocating across a diverse range of opportunities and using asset allocation to support clients on their journey towards their savings goals.